Deductions (Tax Credits) and Limits of Additional Earnings as of 01.01.2023

Childcare Allowance: New Limits for Additional Earnings as of 01.01.2023

The limit for additional earnings for childcare allowance recipients (lump-sum system independent of earnings) will increase from EUR 16,200.00 to EUR 18,000.00 as of 01.01.2023. For recipients of the earnings-related childcare allowance, the limit for additional earnings will increase from EUR 7,600.00 to EUR 7,800.00 per year.

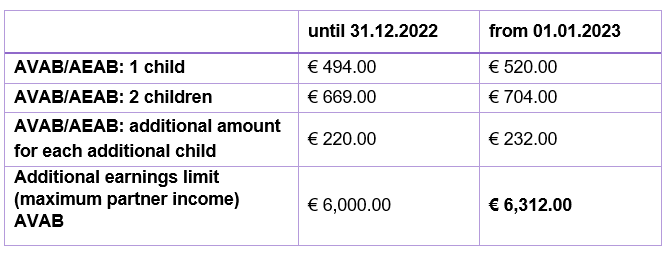

Sole-Earner Deduction/Single-Parent Deduction (AVAB/AEAB) § 33 Abs. 4 Z 1 and 2 EStG 1988

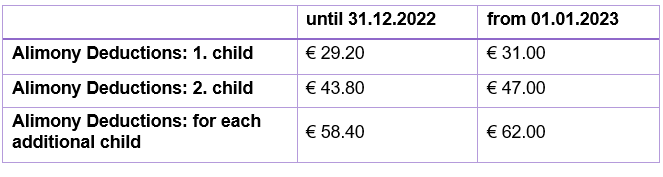

Alimony Deduction § 33 Abs. 4 Z 3 EStG 1988

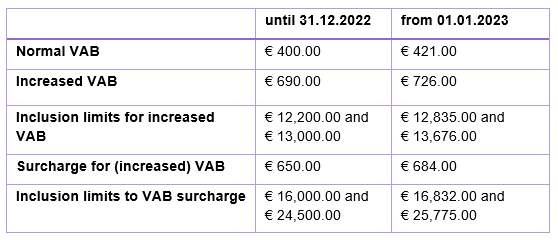

Transportation Deduction (VAB) § 33 Abs. 5 Z 1 - 3 EStG 1988

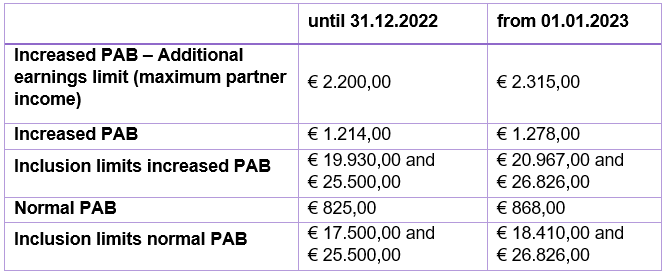

Pension Deduction (PAB) § 33 Abs. 6 EStG 1988

Commuter Allowance in Conjunction with Travel Allowance/Job Ticket

Commuter allowance and reduced public transport ticket regulations up until 31.12.2022

Until 31.12.2022, the following applied: If the employer provided tickets or (partially/fully) reimbursed the costs for public transportation (‘job ticket’), the employee was in most cases not entitled to the commuter allowance. This applied regardless of whether the job ticket could be used for the whole commute or just part of the route.

Commuter allowance in conjunction with travel allowance and job ticket as of 01.01.2023

As of 01.01.2023, the commuter allowance is calculated in a first step without consideration of any public transportation tickets provided/reimbursed by the employer. Subsequently, that amount must be reduced by the value of the public transport ticket.

In case of a one-third commuter allowance claim, the allowance must be divided by three and subsequently reduced by the value of the public transport ticket (the commuter euro must also be divided by three).

The commuter euro is due for the entire distance (home-workplace), even if the commuter allowance is zero due to the deduction of the commuter allowance. If the public transport ticket is available for longer periods than one calendar month, the monthly contribution is determined on a proportional basis.

Mandatory Personal Income Tax Return – Additional Triggers

Inflation Premium

In the year 2022 and 2023, the employer may pay a tax-free and contribution-free inflation premium to their employees of up to € 3,000.00 per employee per calendar year (special payment).

If more than one employer pays an inflation premium within the same calendar year (either parallel employment relationships or consecutive employment relationships), and the sum of the paid inflation premiums exceed the limit of € 3,000.00, the tax-exempt amount of € 3,000.00 must be split between the employments proportionately.

Employees who receive tax-free inflation premiums of more than € 3,000.00 per year are subject to mandatory income tax returns. This is to make sure that any inflation premium exceeding € 3,000 is taxed correctly (taxable income).

The tax-free inflation premium will not affect the entitlement to an early retirement pension. Likewise, the childcare allowance remains unaffected by the granting of a tax-free inflation premium (applicable to both childcare allowance systems: earnings-related or lump-sum).

The inflation premium for 2022 can be paid retroactively until 15.2.2023 (payroll roll-up). This offers a last chance for late filers.

Employee shares

The mandatory PIT return will also be triggered if the sum of tax-free employee shares and tax-free inflation premium exceeds the total amount of € 3,000.00.