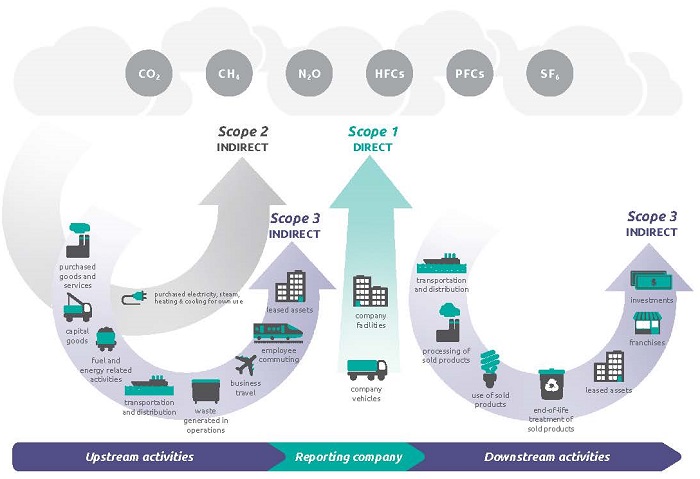

What are Scope 1, 2 and 3 emissions?

Scope 1: Direct emissions that result from activities within your organisation’s control. This might include onsite fuel combustion, manufacturing and process emissions, refrigerant losses or company vehicles.

Scope 2: Indirect emissions from electricity, heat or steam that you purchase and use. Although not directly in control of the emissions, by using the energy you are indirectly responsible for the release of CO2.

Scope 3: Any other indirect emissions from sources outside of your direct control. This category covers all the emissions associated, not with the company itself, but those for which the organisation is indirectly responsible up and down the value chain. This includes purchased goods and services, use of sold goods, business travel, commuting, waste disposal and water consumption.

The terms Scope 1, 2 and 3 emissions were created by the GHG Protocol in 2001, where their meaning is demonstrated in the following graphic:

Overview of GHG Protocol scopes and emissions across the value chain

Source: ghgprotocol.org

Benefits of a well-defined environmental strategy

- Reduces emissions and safeguards the business from rising carbon tax costs

- Reduces energy consumption and protects the business against energy price rises

- Supports alignment with regulations, compliance and aligns to international reporting standards (which includes disclosures around scope 1, 2 and 3 emissions)

- Reduces the negative impact of an organisation to the environment.