COVID 19: Accounting for lease modifications

28 May 2020The COVID-19 pandemic is requiring those responsible for the preparation of financial statements to reconsider whether assumptions and assessments previously made are still valid and appropriate which in turn is creating an additional burden on entities all over the world. In particular, IFRS 16 has become an area of focus for entities and the International Accounting Standards Board (IASB).

The IASB has therefore proposed a practical expedient to provide relief for lessees from lease modification accounting for rent concessions related to COVID-19. In this article we explain the current accounting requirements, the proposed practical expedient and how to apply it.

Download COVID-19 accounting for lease modifications

Lessors are providing lessees with rent concessions. These can be in the form of rent holidays or rent reductions for an agreed timeframe (possibly followed by increased rentals in future periods). In some jurisdictions, governments are making rent concessions a requirement. In others they are merely encouraging them. These concessions will have major impact for some lessees, particularly in the retail and hospitality industries which in many cases have been forced to temporarily close their premises.

IFRS 16 contains specific requirements on accounting for lease modifications. Rent concessions that change the overall consideration for the lease are in the scope of these requirements. Lessees are currently required to assess whether rent concessions are lease modifications and, if they are, apply specific accounting guidance. This can be burdensome, especially for large portfolios of leases with different features and different types of concessions. Entities already have significant pressures upon them as a result of this pandemic and what is set out in IFRS 16 just adds to the burden.

Lessor modifications

Finance leases

Lessor accounting for modification of finance leases is detailed in IFRS 16.79 to 80. Similar to lessee accounting, when the scope of a lease increases and the consideration changes commensurately, a separate lease exists. Where this is not the case, the lessor must:

- reassess the accounting for the lease and determine if the lease would have been considered an operating lease if the modification had been known; and, if so:

- create a new lease from the effective date of the modification; and

- reclassify the lease receivable balance at the date of modification to property, plant and equipment

- where the lease remains a finance lease, the lease receivable is remeasured by the application of IFRS 9. In such a case, assuming that that the receivable is classified as amortised cost, the change in future cash flows is a remeasurement event resulting in a gain or loss within profit or loss.

Operating leases

IFRS 16 provides only limited guidance on modification of operating leases from a lessor’s perspective. It requires that any modification be considered a new lease, and that any remaining prepayments and accruals are included in the accounting for this new lease. IFRS 16 does not state whether balances arising from the lessor’s straight-lining calculation are considered to be accruals or prepayments but our view, consistent with the approach when applying IAS 17, is that they are.

In such an instance, if the new lease continues to be classified as operating, the future cash flows are recognised on a straight line (or other systematic) basis, adjusted for any prepayments or accruals. The expense recognition pattern should ensure the balance is written down to zero at the end of the lease.

Impairment

Due to the change in fair value of future cash flows, impairment indicators may exist such that impairment of the individual assets should be considered.

Lessee modifications

Reassessment vs. modification

Lease modification and reassessment of the lease liability are two different concepts with potentially different accounting outcomes. Generally, a reassessment takes place when there are changes in lease payments based on contractual clauses included in the original contract – such as changes in CPI, a market price adjustment, a change in any price guarantee arrangement that might appear in the lease contract (IFRS 16.42). In such an instance, future cash flows are reforecast and present-valued utilising the discount rate set in the initial measurement of the lease (IFRS 16.43).

A lease modification (as considered in this document – does not address changes in leased asset, such as decreases in leased space) arises when the lease contract is altered such that future cash flows and/or the scope of the lease change. Where an increase in scope occurs, and the payment for this increase in scope is commensurate, a separate lease is accounted for (IFRS 16.44). Otherwise, the original lease is remeasured by:

- identifying a revised discount rate appropriate to the revised lease term, underlying asset and the lessee

- determining the net present value of future cash outflows using that revised discount rate

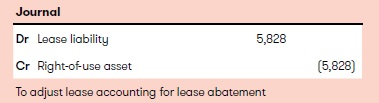

- adjusting the remaining right-of-use asset for the increase or decrease in the lease liability. If the adjustment exceeds the carrying value of the right-of-use asset this excess is recognised as a gain in profit or loss.

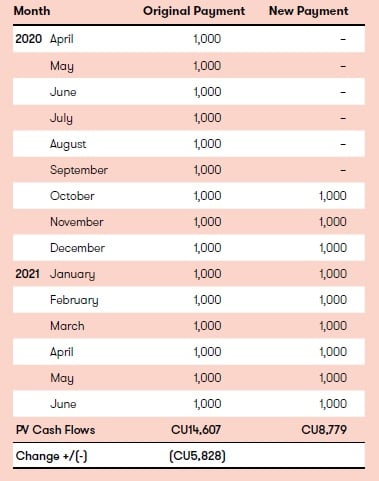

Example 1 - lease abatement

RetailCo closed its stores on 15 March 2020. Economic and regulatory circumstances changed on 30 June 2020 such that RetailCo wished to reopen its stores, however, the significant period of time with no cash inflow resulted in insufficient working capital to meet its lease obligations.

On 1 April 2020, RetailCo received a 6-month lease abatement from its landlord, starting 1 April and expiring 30 September 2020. RetailCo’s incremental borrowing rate was 4% at lease inception; it is now 6% because its credit rating has fallen. Payments were CU1,000 per month, expiring in 30 June 2021. Renegotiated payments remain consistent. Payments are in arrears.

At 1 April 2020, the balance of the right-of-use asset was CU15,000. The Liability balance was CU14,607.

Decrease in lease liability > right-of-use asset

If the right-of-use asset had been CU5,000 at the date of modification, the decrease (CU5,828) is more than the right-of-use asset. In such a case, a gain is recognised:

The proposed practical expedient

The proposed practical expedient bypasses the need for lessees to carry out an assessment to decide whether a COVID-19 related rent concession received is a lease modification or not. The lessee accounts for the rent concession as if the change was not a lease modification. However, there are no proposed changes for lessors.

The proposed practical expedient is only applicable to rent concessions provided as a direct result of the COVID-19 pandemic. In addition, the relief is only proposed for lessees that are granted these rent concessions. All of the following conditions in relation to permitting a lessee to apply the practical expedient need to be met:

- the rent concession provides relief to payments that overall results in the consideration for the lease contract being substantially the same or less than the original consideration for the lease immediately before the concession was provided.

- the rent concession is for relief for payments that were originally due in 2020. So payments included are those that are reduced or deferred in 2020, but any subsequent increased payments can go beyond 2020

- there are no other substantive changes to the other terms and conditions of the lease.

- The IASB is planning to complete any amendments resulting from submissions on this ED by the end of May so the proposed practical expedient can be used in any financial statements that are issued after 1 June 2020.

Earlier application will be permitted, including for financial statements not yet authorised for issue at the date the amendment is issued. This article will be updated when the amendment is issued.

Some practical examples of where the practical expedient might be used are where payments:

- are deferred for a period of time, and then increased at a future date

- are forgiven completely for a period of time

- are partly deferred and partly forgiven, and then partly increased at a future date.

A concession that simply defers rentals payments to a later date is not necessarily a modification based on the IASB’s recent education guidance. The proposals in the ED are however still useful as they avoid the lessee having to assess whether or not modification accounting applies.

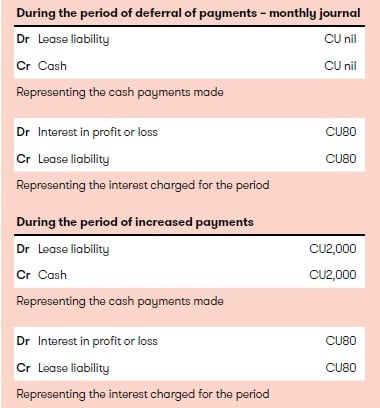

Example 2 - accounting for payments deferred and then increased at a future date

Scenario

A lessee is paying monthly lease payments of CU1,000. The lessor has agreed to defer 6 months of lease payments from 2020 to 2021 as a result of COVID-19. Assume interest accrues at CU80 per month and the 6 months increased lease payments of CU2,000 commence on 1 April 2021 and continue until 30 September 2021.

The lease liability at the end of the period where payments were increased would be the same as if the payments had not been altered at all.

During both periods, in our view, amortisation should be charged on the right-of-use asset as normal.

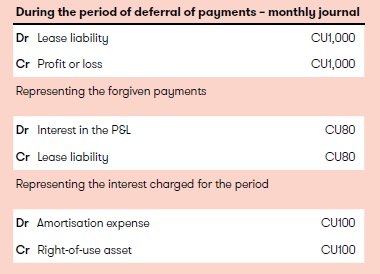

Example 3 - accounting for forgiven lease payments

Scenario

A lessee is paying monthly lease payments of CU1,000. The lessor has agreed to forgive 6 months of payments in 2020 with no adjustment to future rentals. Assume interest accrues at CU80 per month. Monthly depreciation is CU100.

In our view, the preferred presentation of the credit within profit or loss is to follow the accounting policy for variable lease payments. However, we do believe there is an argument to present the credit as a financial item, as ‘debt forgiveness’. As long as it is appropriately disclosed, in our view either treatment would be acceptable.

How Grant Thornton can help

Preparers of financial statements will need to be agile and responsive as the situation unfolds. Having access to experts, insights and accurate information as quickly as possible is critical – but your resources may be stretched at this time. We can support you as you navigate through accounting for the impacts of COVID-19 on your business.

Now more than ever the need for businesses, their auditors and any other accounting advisors to work closely together is essential. If you would like to discuss any of the points raised, please speak to our experts Christoph Zimmel and Rita Gugl.